The Right Way to Tap Your Home Equity for Cash

Table of Content

For a more precise estimate, you can hire a professional real estate appraiser. Andrew Martins is an award-winning journalist who has performed thousands of hours of research on small business products and services and technology. Over the last 12 years, he has also studied and covered taxes, politics, and the economic impacts policy decisions have on small business.

A home equity loan is often referred to as a second mortgage because that's truly what it is. It's a loan that lets you borrow against the value of your home. Often, this type of loan can be a way for homeowners to access large sums of money to pay for life's big expenses. It's not uncommon to see someone take out a home equity loan to finance home improvements, to cover medical debts, or to assist a child in paying for his or her education.

What is a second mortgage?

There may be additional restrictions on the amount you can borrow or loan type you can select if you choose to pay interest only. Choosing to repay principal and interest means that you're actually paying off the total home loan amount over the period of the loan, not just the interest charges. \nIn under 5 minutes, you can get your application started for pre-approval, a new home loan, refinancing, or topping up your existing home loan.

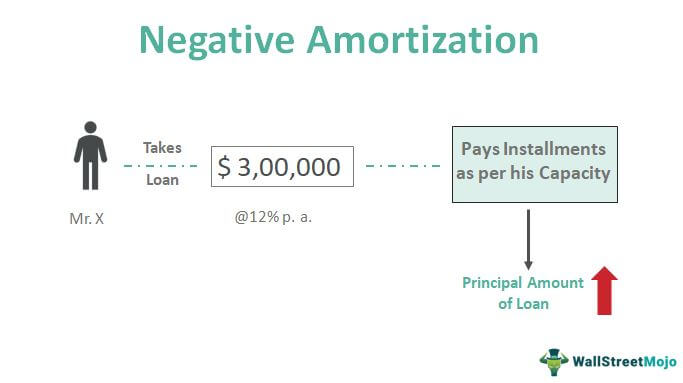

You can then borrow an equity loan to cover from 5% and up to 20% of the property purchase price of your newly built home. Most lenders will want you to have at least 15% to 20% equity in your home both before and after the home equity loan. So, for example, if your home is currently worth $300,000 and you still owe $270,000 on your mortgage, your equity is $30,000, or 10%. In that case, you most likely wouldn't qualify for a home equity loan or HELOC.

Low competitive home equity rates — plus:

If the plan does not allow renewals, the borrower will not be able to borrow additional money once the period has ended. Some plans may call for payment in full of any outstanding balance at the end of the period. Others may allow repayment over a fixed period, for example, ten years. A home equity loan is worth considering if you have a large, one-time expense, or if you want to consolidate debt and focus on paying it off. It offers fixed rates and a steady repayment schedule for the life of the loan.

If you itemize deductions, you may be able to deduct interest accrued on a home equity loan. Consult a tax professional for guidance on your personal tax situation. If you’d prefer to increase your overall savings rate instead, you’ll need to tighten up your discretionary spending, pursue a side hustle, or find passive income opportunities. However, if you’re banking on your project’s resale value boost to offset your investment, it’s crucial to calculate the likely value-add. That’s doubly true if you’re planning to turn around and sell your home soon after completing the project. In this scenario, you wait to apply for your loan until your project’s first bills arrive.

Loan Collateral and Terms

A HELOC may be used, repaid, and reused for as long as the account stays open, which is typically 10 to 20 years. A personal loan is probably the best way to go for those who need to borrow a relatively small amount of money and are certain they can repay it within a couple of years. A personal loan calculator can be a useful tool for determining what kind of interest rate is within your means.

It’s important to weigh up the pros and cons of different scenarios before making a decision. It’s important to understand that your total equity isn’t necessarily all available for you to use. A lender calculates usable equity as 80% of the value of the property minus the loan balance. A simple way of understanding the concept is to imagine that you sell your current home or investment property today and pay off your mortgage in full – equity is the amount of money you’d have left over. This feature will allow you to email a summary of your results to yourself or share it with someone else.

Estimated repayments and repayment scenario comparisons are estimates only based on the loan amounts, loan types and loan terms selected. The comparisons are indicative estimates for illustrative purposes only and are based on current interest rates . The interest rate for your loan is the rate that applies on the day the loan is drawn down, not the time of application – so it can change. You could apply to lock in a fixed rate for 90 days on fixed rate loans with a fixed term of years (terms and conditions and fee of $750 per $1m in lending apply).

A cash-out refinance refers to using your equity to get a new mortgage that's larger than the amount owed on your existing mortgage. Then, you pay off the existing mortgage and use the remaining money as needed. As with home equity loans and lines of credit, the funds are tax free because they're viewed as debt by the IRS, not income. A home equity loan is usually a fixed-rate loan distributed in one lump sum, with terms that range from 5 to 30 years. This might be a good loan if you anticipate a large one-time expense such as a wedding, the purchase of a second home, or debt consolidation. A fixed rate and predictable monthly payment can help you budget as you work toward your financial goals.

Determine the current balance of your mortgage and any existing second mortgages, HELOCs, or home equity loans by finding a statement or logging on to your lender’s website. Estimate your home’s current value by comparing it with recent sales in your area or using an estimate from a site like Zillow or Redfin. Be aware that their value estimates are not always accurate, so adjust your estimate as needed considering the current condition of your home. Then divide the current balance of all loans on your property by your current property value estimate to get your current equity percentage in your home. You’ll find home equity loan rates are often higher than interest rates on traditional mortgages. The more home equity you borrow, the higher your rate will typically be.

Every lender is different, so take the time to get several home improvement loan quotes from multiple lenders. You can get prequalified in minutes and receive quotes from multiple lenders. However, an owner can leverage their home equity as collateral in a variety of ways to secure low-cost funds for their financial needs. Unlike some investments, home equity cannot be quickly converted into cash. That's because the equity calculation is based on a current market value appraisal of your property. That appraisal is no guarantee that the property would sell at that price.

Comments

Post a Comment