HELOC vs Home Equity Loan vs Personal Loan UW Credit Union

Table of Content

As you withdraw money from your HELOC, you’ll receive monthly bills with minimum payments that include principal and interest. Payments may change based on your balance and interest rate fluctuations, and may also change if you make additional principal payments. Making additional principal payments when you can will help you save on the interest you’re charged and help you reduce your overall debt more quickly. A HELOC has a variable interest rate, so payments fluctuate based on how much borrowers are spending in addition to market fluctuations. This can make a HELOC a bad choice for individuals on fixed incomes who have difficulty managing large shifts in their monthly budget.

HELOCs may sound sweet, but all that free-flowing cash doesn’t come without risks. If you don’t pay off your HELOC under the terms you’ve agreed to, the lender can foreclose on your home. It doesn’t matter how much you’ve paid on your first mortgage; a HELOC can be lethal.

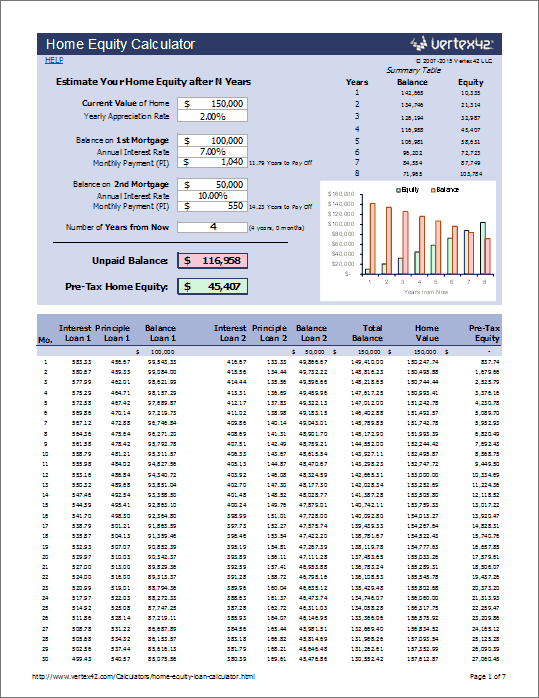

How to Calculate Your Home Equity

Banks also refer to it as a repayment period which is usually 30 years. During the repayment phase, a person cannot borrow additional amounts. A HELOC is a revolving line of credit that works like a credit card — except it’s secured by your home. Affordable – On average, personal loans have significantly lower interest rates than credit cards, making them a great option for those looking to consolidate high-rate debt. While this credit union has flexible membership requirements, you still have to join to get a HELOC.

However, this type of loan also comes with risks to keep in mind, such as the possibility of losing your home if you don’t keep up with your monthly payments. During the draw period, you make payments toward your balance, and you can draw funds up to your available limit. When the draw period ends, the repayment period begins, and it’s your responsibility to pay off the balance before the maturity date.

Home Equity Loan vs. HELOC: What’s the Difference?

A hybrid HELOC allows homeowners to borrow up to 80% of the home’s value. Hybrid HELOCs are more like mortgages, as a portion amortizes, which means it requires payments of both principal and interest. Like second mortgages and HELOCs, cash-out refinances have their own credit, LTV and DTI requirements. Generally, you can expect to need a minimum 620 credit score, a DTI less than 50% and a max LTV of 80%. Let’s go back to our first example one more time, with your $250,000 home and $180,000 balance.

If you’re going to be using the money to improve or even increase the value of your home, it can make sense to tap into your home’s existing equity using a HELOC. See expert-recommended refinance options and customize them to fit your budget. HELOCs can be useful financial tools, but they’re not ideal for every financial situation. Here are the most important disadvantages and advantages to be aware of before applying for a HELOC loan so you can make the best choice for your needs. This is because lenders want you to have a certain amount of equity in the home, since you’re less likely to default if you could possibly lose the equity you’ve built up. If the HELOC isn’t what you expected or wanted, don’t sign the financing.

Jobs and Making Money

Find out the conditions under which you can get a home equity loan tax deduction. The equity in your home that you build up over time is precious and worth protecting. However, emergencies might arise when you need to tap into the equity to see you through, or your home might need renovations. The five examples outlined in this article don’t rise to that level of importance. Although home improvement remains the top—and the best—reason for tapping home equity, homeowners must not forget the hard lessons of the past by taking out money for just about any reason.

In most cases, you’re limited to borrowing a total of 85% of your home’s value, according to the Federal Trade Commission . Homeowners sometimes use the terms home equity loan and home equity line of credit interchangeably, but they are very different from each other. Yarilet Perez is an experienced multimedia journalist and fact-checker with a Master of Science in Journalism. She has worked in multiple cities covering breaking news, politics, education, and more. Her expertise is in personal finance and investing, and real estate. As a rule of thumb, lenders will generally allow you to borrow up to percent of your available equity, depending on the lender and your credit and income.

To calculate the equity on your home, subtract the amount owed in mortgage loans for the home from the current appraisal value of the home. You can then express this as a percentage of the appraisal value of the home to compare with the 20%. You can calculate home equity by subtracting the amount owed due to the mortgage from the current estimated value of the house. You may also make use of our Home Equity Line of Credit Calculator to determine further how much you can borrow based on your current home equity. Simple – Your loan's rate, term and amount of the loan are all fixed, so you can rest easy knowing your payments will stay the same and your rate won’t go up. Stable – Your loan’s rate, term and amount are all fixed, so you can rest easy knowing your payments will stay the same and your rate won’t go up.

Good credit opens many doors, especially in the world of lending. If you're interested in leveraging your home equity for a cash loan, you'll need good credit. If you want a better interest rate on that loan, you'll need excellent credit. Before applying for a home equity loan, pull your credit reports and see where you stand. If your credit score is less than desirable, you can fix it yourself.

Conversely, HELOCs allow a borrower to tap into their equity as needed up to a certain preset credit limit. HELOCs have a variable interest rate, and the payments are not usually fixed. Because both home equity loans and HELOCs use your home as collateral, they usually have much better interest terms than personal loans, credit cards, and other unsecured debt.

They are taken out for a set amount and paid back on a regular basis, according to a fixed interest rate. That may make lines of credit less appealing now, as the Federal Reserve embarks on a cycle of raising interest rates several times over the next few months and years. A home equity line of credit offers homeowners access to cash when they need it and requires that interest be paid only on what’s used, based on the appraised value of their homes. A home equity calculator can provide a glimpse of how much you can borrow.

And be sure to avoid any lender who promises one deal when you apply, but gives you a different set of terms to sign, with no good explanation of the change. Never work with a lender who wants you to lie on a financing application — like saying your income is higher than it really is. No matter what large expenses you may face in the future, a home equity line of credit from Bank of America could help you achieve your life priorities. Ebony Howard is a certified public accountant and a QuickBooks ProAdvisor tax expert.

Comments

Post a Comment